Refer to Figure 4-22. What Is the Equilibrium Price in This Market?

Principal Body

Module 10: Marketplace Equilibrium – Supply and Need

The Policy Q uestion: South hould government provide public marketplaces?

In the Capitol Hill neighborhood of Washington, D.C., the Eastern Market is a big building and grounds, owned and operated by the urban center government. Farmers, bakers, cheese makers and other merchants of food, arts and crafts assemble there to sell their wares. Marketplaces like information technology were once a common feature of cities in the U.s.a. and Europe, simply are now a relative rarity. Many accept disappeared as citizens question government back up of marketplaces.

So why does the government play a office in providing some markets? The answer is found in the way markets create benefits for the citizens they serve. In this module, nosotros explore how prices and quantities are set in market equilibrium, how changes in supply and demand factors cause market equilibrium to conform and how we measure the do good of markets to social club.

Markets are often private in the sense that the regime is not involved in their cosmos or presence; instead they are generated by the desire of private individuals to appoint in an exchange for a particular adept. Sometimes, however, the government plays an active role in establishing and managing markets. At the stop of the module we will study why this occurs, using the Eastern Market as an example.

Exploring the Policy Question

Is public investment in marketplaces justified and if so why?

x.ane What is a Market?

Learning Objective 10.one: Place the characteristics of a market.

10.2 Market Equilibrium – The Supply and Demand Curves Together

Learning Objective 10.ii: Determine the equilibrium price and quantity for a marketplace, both graphically and mathematically.

10.3 Excess Supply and Demand

Learning Objective 10.3: Calculate and graph excess supply and excess demand.

x.4 Measuring Welfare and Pareto Efficiency

Learning Objective 10.4:

Summate consumer surplus, producer surplus, and deadweight loss for a market.

ten.v P olicy Example :

S hould Regime Provide Public M arketplaces?

LO 10.five: Employ the concept of economical welfare to the policy of publicly-supported marketplaces.

10.one What is a Market place?

LO 10.1: Identify the characteristics of a market.

In Module 9 nosotros found out where the market place supply curve comes from – the cost structure of individual firms, which in turn comes from their applied science as we discovered in Module 7. In Module v we found out where the need curve comes from – the individual utility maximization issues of individual consumers. In both cases we causeless the demand for and supply of a specific adept or service. In other words we were describing a detail market.

A market is characterized by a specific skillful or service being sold in a particular location at a divers time. So, for instance, we might talk about:

- the market for eggs in Nashville, Tennessee in April of 2016.

- the market for rolled aluminum in the U.S. in 2015.

- the market for radiological diagnostic services worldwide in the last decade.

In improver, for whatever item, time and identify nosotros describe there must be both buyers and sellers in order for a market to exist. A market is where buyers and sellers substitution or where there is both need and supply.

Nosotros tend to talk about markets somewhat loosely when studying economics. For example, we might discuss the market place for orangish juice and leave the fourth dimension and identify undefined in order to go on things simple. Or nosotros might just say that we are looking at the marketplace for denim jeans in the U.S. The difficulty with these simplifications is that we can lose sight of the basic assumptions nigh markets that are necessary for our assay of them.

The six necessary assumptions for markets are the following:

- A market is for a single good or service.

- All goods or services bought and sold in a marketplace are identical.

- The good or service sells for a single price.

- All consumers know everything nigh the production including how much they value it.

- There are many buyers and sellers and they are known to each other and can interact.

- All the costs and benefits of a transaction accrue only to the buyers and sellers who appoint in it.

These assumptions are actually pretty easy to sympathize. They guarantee that the buyers who value the good more than information technology costs sellers to produce it will find a seller willing to sell to them. In other words at that place are no transactions that don't happen because the buyer doesn't know how much he or she likes the product or considering a buyer can't discover a seller or vice-versa.

Of course, the assumptions describe an ideal market place. In reality, many markets are not exactly like this, and subsequently, in Section 7, we volition examine what happens when these assumptions neglect to concord.

x.2 Market Equilibrium: The Supply and Demand Curves Together

LO x.2: Determine the equilibrium price and quantity for a market, both graphically and mathematically.

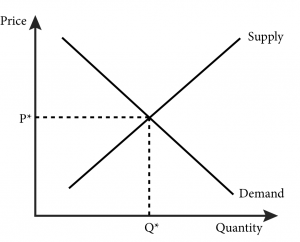

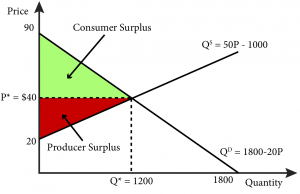

Market equilibrium is the indicate there the quantity supplied by producers and the quantity demanded by consumers are equal. When we put the need and supply curves together we can make up one's mind the equilibrium price: the price at which the quantity demanded equals the quantity supplied. In Figure 10.2.1 the equilibrium price is shown as P* and it is precisely where the need curve and supply curve cross. This makes sense–the demand curve gives the quantity demanded at every price and the supply curve gives the quantity supplied at every price so there is one price that they have in mutual, which is at the intersection of the ii curves.

Figure 10.2.1: The Supply and Demand Curves and Market Equilibrium

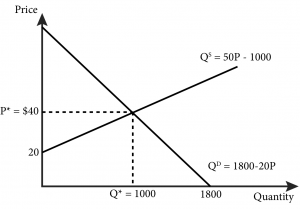

Graphing the supply and demand curves to locate their intersection is one fashion to find the equilibrium price. We tin can also find this quantity mathematically. Consider a demand curve for stereo headphones that is described past the following part:

Q D = 1800 – 20P

Note that in general we draw graphs of functions with the contained variable on the horizontal centrality and the dependent variable on the vertical centrality. In the case of supply and demand curves, even so, nosotros draw them with quantity on the horizontal axis and price on the vertical. Because of this, it is sometimes easier to express the demand relationship as an changed need curve: the demand curve expressed as cost equally a function of quantity. In our example this would exist:

P = 90 – 0.05Q D

This is just the original demand curve solved for P instead of Q D . In the inverse demand bend the vertical intercept is piece of cake to run across from the equation: need for headphones stops at the price of $ninety. No consumer is willing to pay $90 or more for headphones.

Similarly the supply curve can be represented equally a mathematical role. For case, consider a supply curve described by the role:

Q S = lP – 1000

Like to the demand curve nosotros can express this as an inverse supply bend: the supply curve expressed every bit toll as a role of quantity. In this case, the changed supply curve would be:

P = twenty – 0.03Q S

Here the vertical intercept, $xx, gives the states the minimum toll to get a seller to sell headphones. At prices of $20 or less, there will be no supply. So we know that the equilibrium price should be between $20 and $90.

Solving for the equilibrium price and quantity is just a matter of setting Q D = Q S and solving for the cost that makes this equality happen. On our example setting Q D = Q S yields:

1800 – 20P = 50P – 1000

or

lxxP = 2800

or

P = $forty

At P = $40, the quantity demanded and supplied tin be establish from the demand and supply curves:

Q D = 1800 – 20(40) = 1000

Q S = 50(twoscore) – grand = 1000

That these ii quantities match is no blow, this was the condition we set at the outset – that quantity supplied equals quantity demanded. Then we know that a price of $twoscore per unit of measurement is the equilibrium price.

These supply and demand curves for headphones are graphed in Effigy 10.2.2 below, and their intersection confirms the equilibrium price we calculated mathematically.

Figure ten.two.2: Explicit Supp ly and Demand Curves for Headphones

Note that we have also identified the equilibrium quantity , Q*—the quantity at which supply equals demand. At $40 per unit of measurement, thou headphones are demanded and exactly g headphones are supplied. The equilibrium quantity has nothing to do with whatsoever kind of coordination or communication amid the buyers and sellers; it has only to do with the price in the market. Seeing a unit price of $forty, consumers demand chiliad units. Independently, sellers who see that price will choose to supply exactly 1000 units.

ten.3 Excess Supply and Demand

LO 10.three: Calculate and graph backlog supply and excess need.

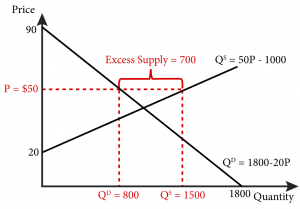

It makes sense that the equilibrium price is the ane that equates quantity demanded with quantity supplied, just how does the market get to this equilibrium? Is this just an blow? No. The market place price will automatically conform to a indicate where supply matches demand. Excess supply or demand in a market will trigger such an adjustment.

To understand this equilibrating characteristic of the market place cost, allow's return to our headphones example. Suppose the price is $50 instead of $40. At this price nosotros know from the supply bend that 1500 units will be supplied to the market. As well, from the demand curve, we know that 800 units will exist demanded. Thus there volition be an excess supply of 700 units, as shown in Effigy 10.2.3.

Excess supply occurs when, at a given cost, firms supply more of a good than consumers demand. These are goods that have been produced by the firms that supply the marketplace that have not found any willing buyers. Firms will want to sell these goods and know that past lowering the price more buyers will announced. So this backlog supply of appurtenances will atomic number 82 to a lowering of the price. The toll will go along to fall as long every bit the excess supply weather be. In other words, price will continue to fall until information technology reaches $twoscore.

Figure 10.2.3: Excess Supply of Headphones at a Price of $50

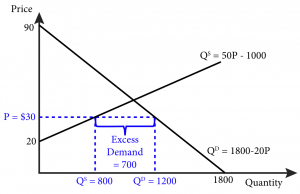

The same logic applies to situations where the price is below the intersection of supply and need. Suppose the price of headphones is $30. We know from the demand curve that at this price, consumers will demand 1200 units. We as well know from the supply curve that at this price suppliers will supply 500 units. And then at $30 in that location will be excess demand of 700 units, every bit shown in Figure 10.two.three.

Backlog need occurs when, at a given toll, consumers demand more of a good than firms supply. Consumers who are not able to find goods to purchase volition offer more money in an effort to entice suppliers to supply more. Suppliers who are offered more than coin will increase supply and this will continue to happen as long as the price is below $40 and in that location is excess need.

Figure 10.2.3 b: Excess Demand for Headphones at a Price of $3 0

Only at a price of $forty is the pressure for prices to rise or fall relieved and volition the price remain constant.

10.4 Measuring Welfare and Pareto Efficiency

LO ten.4: Summate consumer surplus, producer surplus, and deadweight loss for a market place.

From our study of markets so far, information technology is clear that they can contribute to the economic well-being of both buyers and sellers. The term welfare, equally it is used in economics, refers to the economical well-existence of guild as a whole, including producers and consumers. We can measure welfare for particular marketplace situations.

To sympathize the economic concept of welfare—and how to quantify it–it is useful to call up nigh the weekly farmers' market in Ithaca, New York. The market is a place where local growers can sell their produce directly to consumers throughout the summer. It is very successful and many local residents get to the market place to buy produce. Now consider the specific example of tomatoes. What is this market worth to the love apple sellers and buyers that transact in the market place?

Suppose a farmer has a minimum willingness-to-accept toll of $one for an heirloom lycopersicon esculentum. This price could be based on the farmer'south toll of product or the value she places on consuming the tomato herself. Suppose as well that at that place is a consumer who really wants an heirloom love apple to add to his salad that evening and is willing to pay up to $three for ane. If these two people see each other at the market and agree on a price of $ii, how much benefit do they each get?

The seller receives $2 and it price her $one to provide the tomato plant, so she is $one improve off, the deviation betwixt what she received and what she would have accustomed for the tomato. Besides, the heir-apparent pays $2 but receives $3 in benefit from the tomato, since that was his willingness to pay; his net benefit is the difference, or $one. The seller and buyer are both $1 better off because they had the opportunity to run into and transact. Without this opportunity the seller would accept stayed at home with the tomato and been no ameliorate or worse off, and the buyer would not take a tomato plant for his salad just would exist no better or worse off.

The difference between the price received and the willingness-to-accept price is called the producer s urplus ( PS ). The difference between the willingness-to-pay toll and the price paid is called the consumer surplus ( CS ). The sum of these two surpluses is called full surplus ( TS ). So the producer surplus in the tomato plant example is $1, the consumer surplus is $1 and the full surplus is $2. This is the surplus generated by the one transaction; if we add up all such transactions in the market we get a measure of the consumer and producer surplus from the market place.

Quantifying surplus for an entire market is easy to do with a graph. Let'due south return to our previous example of headphones and detect the consumer and producer surplus.

Figure 10.4.1 shows that the consumer surplus is the expanse above the equilibrium price and below the demand curve –the green triangle in the figure. Similarly, the producer surplus is the area below the equilibrium cost and above the supply curve –the red triangle in the figure. The expanse of each surplus triangle is easy to calculate using the formula for the area of a triangle: ½bh , where b is base of operations and h is summit.

Figure ten.4.one: Consumer Surplus and Producer Surplus in the Market for Headphones

In the instance of consumer surplus the triangle has a base of grand, the distance from the origin to Q*, and a meridian of $fifty, the difference betwixt $ninety, the vertical intercept and P*, which is $40.

Consumer surplus = ½(yard)($l) = $25,000

Similarly,

Producer surplus = ½(m)($20)= $10,000

Total surplus created past this market is the sum of the two or $35,000. This is the measure of how much value the marketplace creates through its enabling of these transactions. Without the ability to come together in this market the buyers and sellers would miss out on the opportunity to capture this surplus.

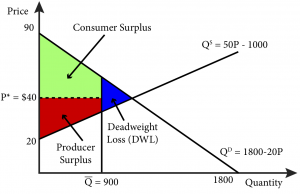

Nosotros say that a market is efficient when the entire potential surplus has been created. Such a market is an instance of Pareto efficiency — an allocation of goods and services in which no redistribution can occur without making someone worse off. Think about the distribution of goods in the headphones example. All of the buyers and sellers that transact are made better off past the transaction considering they gain some surplus from it. If they didn't, they would not voluntarily trade. None of the trades that shouldn't happen do. For example if at that place were more than one thousand units exchanged it would mean sellers were selling to buyers who valued the good less than the sellers' cost of production, where the supply bend is in a higher place the need curve, and ane or both of the parties would be worse off because of the exchange.

Another way to see that the market equilibrium effect is efficient is if we arbitrarily limit the number of goods exchanged to 900. Allow's phone call this maximum quantity restrictionQ̅, where the bar to a higher place the Q indicates that it is fixed at that quantity. There are 100 surplus-creating transactions that don't occur; this cannot exist an efficient outcome because the entire potential surplus has non been created. The lost potential surplus has a proper name, dead weight loss ( DWL ): the loss of total surplus that occurs when at that place is an inefficient allotment of resources. The blue triangle in Figure 10.4.2 represents this deadweight loss.

Figure 10.4.ii: Deadweight loss from a quantity constraint

We can calculate the value of the deadweight loss precisely, again using the formula for the area of a triangle. Since the need function is Q D = 1800 – 20P, the signal on the need curve that results in a demand of 900 is a price of $45. Similarly the supply function is given as Q S = lP – 1000, the point on the supply bend that results in a quantity supplied of 900 is a price of $38. Thus the base of the triangle is $45-$38 or $seven and the height is the difference betwixt the m units that sold in the absence of a restriction and the 900 unit restricted quantity or 100. So DWL = ½($7)(100) = $350.

x.5 Policy Example : S hould Government Provide Public Thou arketplaces?

LO 10.5: Apply the concept of economical welfare to the policy of publicly-supported marketplaces.

The beginning question in determining whether a case can be fabricated for the public provision of marketplaces, such as the Eastern Marketplace in Washington, D.C., is what would occur in the absence of such a marketplace. If the buyers and sellers in these markets could easily admission other markets and so it would be difficult to fence that the market place is providing a internet benefit. Similarly, if the commercial activity that takes place in this market place is simply a diversion of similar activity that would have taken identify elsewhere, then it is likely that at that place is little to no net benefit. And so, for the sake of this do, we volition assume that the marketplace is providing an opportunity to these buyers and sellers that they would non otherwise have.

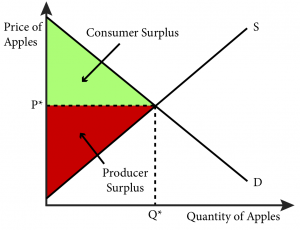

Then, given this assumption, are these marketplaces valuable? The elementary answer, as long as transactions are occurring, is yes. Nosotros tin can run into this from a simple diagram of an individual appurtenances market, let's say for fresh apples, that exists within the Eastern Market place (Figure ten.5.1).

Figure ten.5.1: The Marketplace for Apples in t he Eastern Market

There is clearly surplus beingness created past the apple transactions that take place within the market. This in itself is the primary statement for the marketplace. Buyers and sellers are able to transact and become better off for it. The value to those individuals is measured by surplus.

Simply a complete answer must compare the value to gild of the markets to the cost to society of the marketplace itself. Does the full surplus created by the market justify the price?

Let'south return at present to the fundamental assumption – that a marketplace for fresh apples would not exist without government back up. Is this a reasonable supposition?

In the 19th and early 20th centuries when many public markets were founded, transportation was difficult and bringing fresh food to support urban population centers was something local governments ordinarily did. Today, transportation is non nearly as hard or costly. But although many areas are well served by grocery stores, where information technology is reasonable to wait customers volition notice fresh fruits and vegetables, other locations are characterized by nutrient deserts:

Food deserts are divers as urban neighborhoods and rural towns without ready access to fresh, healthy, and affordable food. Instead of supermarkets and grocery stores, these communities may take no food access or are served only by fast food restaurants and convenience stores that offer few healthy, affordable food options. The lack of access contributes to a poor diet and tin lead to higher levels of obesity and other diet-related diseases, such as diabetes and heart disease. (U.S. Department of Agriculture (USDA))

The USDA estimates that 23.v million people in the U.s. live in food deserts.

Although the Capitol Hill neighborhood experienced some hard times in the by, today it is prosperous and well served by grocery stores. So the need for government support of the Eastern Market there is less clear. In Section vii we will explore public goods and externalities in detail and become better equipped to fully explore this issue.

Exploring the Policy Question

- What other kinds of marketplaces can you think of that the authorities aids by providing infrastructure?

- Airports let the marketplace for airline travel to be in a functional manner. Most airports in the United States are run past local governments. Using the topics explored in this module, requite a justification for government expenditures on airports.

- Should the District of Columbia regime spend money on a market that primarily serves one neighborhood? Give reasons for and against.

SUMMARY

Review: Topics and Related Learning Outcomes

x.1 What is a Market?

Learning Objective 10.1: Place the characteristics of a market.

10.ii Market Equilibrium – The Supply and Need Curves Together

Learning Objective 10.2: Determine the equilibrium toll and quantity for a market place, both graphically and mathematically.

x.3 Excess Supply and Need

Learning Objective 10.3: Calculate and graph backlog supply and backlog need.

ten.iv Measuring Welfare and Pareto Efficiency

Learning Objective 10.4:

Calculate consumer surplus, producer surplus, and deadweight loss for a market.

10.5 Policy Example:

S hould Government Provide Public M arketplaces?

LO 10.5: Utilise the concept of economic welfare to the policy of publicly-supported marketplaces.

Acquire: Primal Terms and Graphs

Terms

Market Equilibrium

Inverse Demand Bend

Inverse Supply Curve

Equilibrium Price

Equilibrium Quantity

Backlog Demand

Backlog Supply

Producer Surplus

Consumer Surplus

Total Surplus

Pareto efficiency

Deadweight loss

Graphs

The Supply and Demand Curves and Market place Equilibrium

Explicit Supply and Need Curves

Excess Supply at a Cost of $l

Excess Demand at a Price of $30

Consumer Surplus and Producer Surplus

Deadweight loss from a quantity constraint

A Typical Goods Market in The Eastern Market

Equations

Quantity supplied

Quantity demanded

Source: https://open.oregonstate.education/intermediatemicroeconomics/chapter/module-10/

0 Response to "Refer to Figure 4-22. What Is the Equilibrium Price in This Market?"

Post a Comment